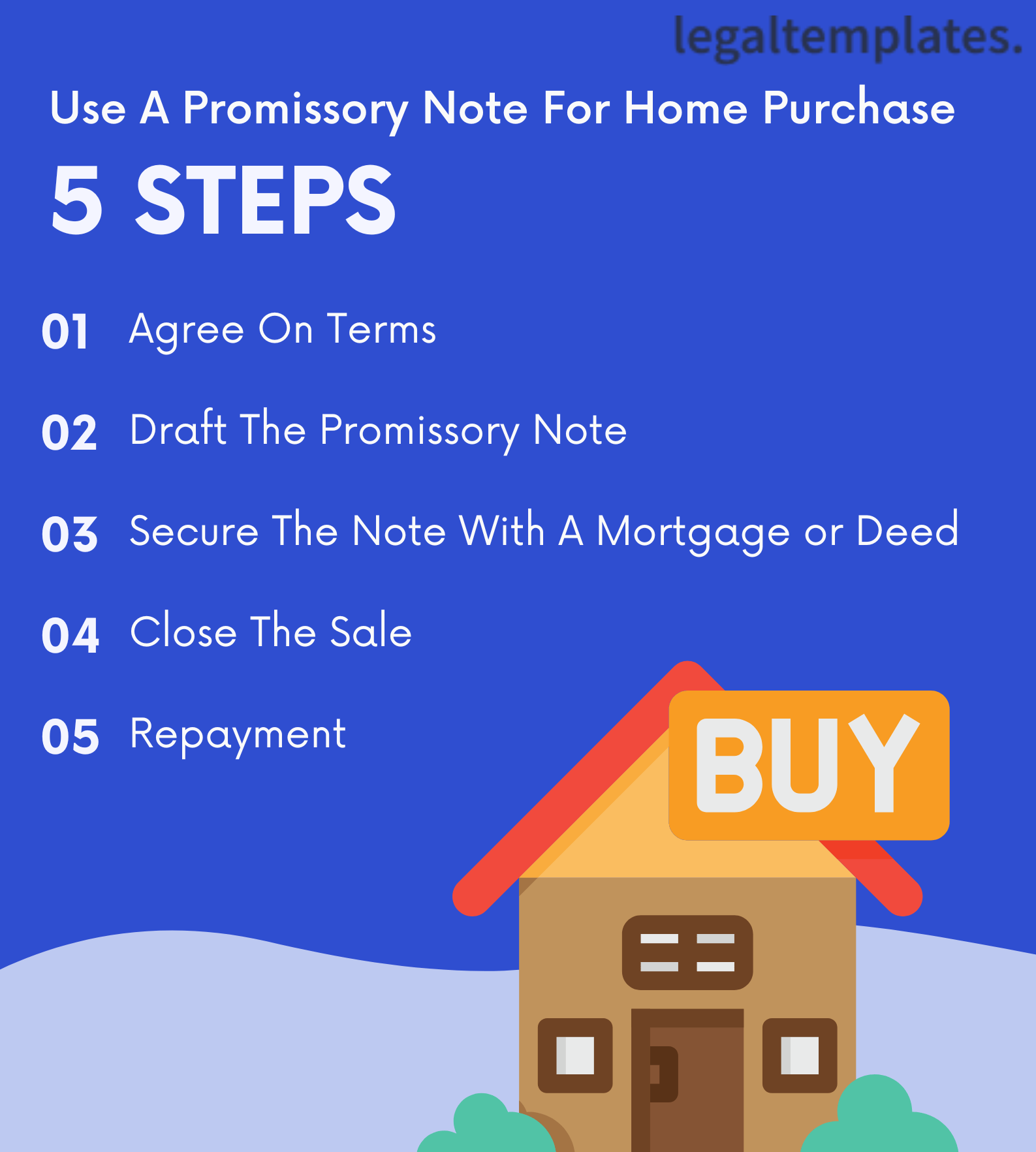

Promissory notes are legal documents used in real estate transactions to establish the terms and conditions of a loan for real estate property. They formalize the borrower’s promise to repay the real estate loan within the terms provided.

Understanding how they work in real estate transactions can help borrowers and lenders protect their legal interests and avoid unnecessary complications.

A promissory note in real estate acts as a legally binding agreement between the lender and borrower. It typically includes the loan amount, details about repayment, and consequences in the event of default.

Real estate loans generally include a promissory note or loan agreement and a mortgage or deed of trust.

The primary difference between a promissory note, a mortgage, or other real estate financial instrument is its intent. A mortgage or deed of trust enforces a promissory note, establishing consequences for non-payment by using the property as collateral for the loan. If the borrower defaults on the loan agreement, the lender can use the mortgage or deed of trust to take possession of the property and sell it to recover the loan value.

Once the loan is satisfied, the lender provides a release, and the property belongs to the borrower, free and unencumbered.

There are four primary types of promissory notes in real estate. They may be secured or unsecured and have adjustable or fixed-rate interest.

The primary difference between secured and unsecured promissory notes is collateral.

Secured: Use collateral, often the property itself, to ensure payment by the borrower. The lender takes possession if the borrower fails to meet the note terms. The lender may also accept different property, such as a vehicle, as collateral instead.

Unsecured: Does not use collateral to ensure loan repayment. Should the buyer default, the lender may pursue collections or sue the buyer to recover the property value.

Adjustable rate and fixed rate notes apply different interest rate terms.

Adjustable rate: Allows for changes to the interest rate and monthly payment. Adjustable rates are ideal for real estate transactions when the buyer expects to pay the loan off or sell before the interest rate increases.

Fixed-rate: Establishes a set interest rate and monthly payment amount. This reduces the risk for the buyer, who can make a repayment plan without unanticipated changes.

Each real estate promissory note has different details based on your transaction, but most include the following:

Promissory notes are often part of a larger real estate financing plan. The most common uses in real estate include the following.

Most traditional mortgages include a secured note. The note acknowledges that the borrower is responsible for repaying the loan from a bank or lending institution. It consists of the amount and terms of repayment and, with the mortgage agreement, outlines the penalties for default.

Usually, a traditional mortgage allows the lender to take ownership of the financed property if the borrower fails to meet the payment terms agreed to in the note.

Sometimes, the seller of a property may not choose to go through a bank or lending institution. Instead, they will finance the purchase directly through seller financing. Seller financing allows the seller to receive payment for the real estate property directly from the buyer.

A clear, detailed promissory note is critical for seller financing. It is the primary payment agreement between the buyer and seller and should include loan terms, payment amounts, and interest rates. A promissory note for seller financing should address the penalties and remedies for late payments and non-payment.

When purchasing real estate, the buyer may not use a mortgage but instead opt for a private loan. This could be through a banking institution or other lender. As with other real estate purchase options, a promissory note ensures both parties know the loan repayment amounts, terms, and interest rates.

Private loans for real estate often arise when the real estate value is too low for a traditional mortgage, or the buyer does not have sufficient assets or credit to qualify for a mortgage.

Promissory notes provide critical legal documentation that benefits lenders and borrowers in real estate transactions.

Advantages for borrowers include:

Advantages for lenders include:

Promissory notes facilitate real estate purchases and home loans by promising the lender payment on specific terms. The note establishes a legally binding contract between a borrower and lender for repayment. They are often incorporated into real estate transactions when the borrower does not qualify for a traditional mortgage loan through a lending institution.

They detail the loan agreement, including the principal, repayment amount, and interest. A promissory note may be used with a mortgage, deed of trust, or loan agreement. The lender and the borrower sign to make it a legally binding agreement.

Unlike a mortgage or deed of trust, the note does not necessarily allow the lender to take possession of the property or other named collateral in the event of default. Unless otherwise specified, it does not typically allow the lender to foreclose on the property to recover their investment. Instead, the lender can sue the defaulting borrower to recoup the loan value.

Whether you are a borrower or lender, you benefit from understanding the legal implications, protections, and state-specific laws governing promissory notes before signing a real estate loan.

Since a promissory note is a legal and binding agreement, it offers some protection for both the lender and the borrower. A signed, documented payment agreement allows both parties to hold the other accountable if there is a disagreement.

A promissory note can ensure the buyer takes ownership of the property when they satisfy the loan agreement terms. At the same time, the note provides guidelines for loan repayment and outlines consequences. This protects the lender, who has legal grounds to sue the borrower if they default.

Promissory notes in real estate transactions present a greater risk for the lender, especially when they are unsecured by a mortgage or other security instrument. Even if they sue for non-payment, the lender could lose financially if the borrower defaults and has no assets to cover the loan value. They may mitigate this loss by requesting a higher down payment or negotiating a higher interest rate.

Some lenders try to protect themselves by establishing a forfeiture clause. In the event of default, a forfeiture clause allows the lender to retain the property and any payments made on the promissory note up to that point. Many states will not uphold a forfeiture clause.

Legal Content Editor

Josh Sainsbury is a business content editor at LegalTemplates. His background in a variety of industries allows him to create legal content that’s accessible and understandable for all audiences.